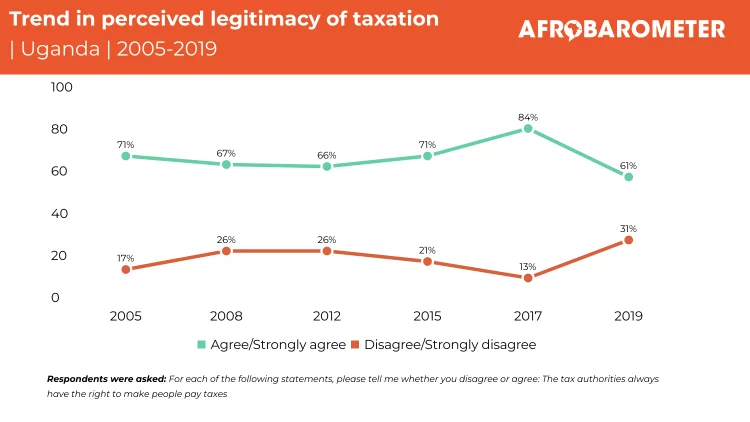

- Perceived legitimacy of taxation: Six in 10 Ugandans (61%) say their government has the right to make people pay taxes. But this support has declined by 23 percentage points since 2017.

- Perceived fairness of the tax system: About two-thirds (65%) of Ugandans say ordinary people have to pay too much in taxes. Only half as many (33%) say the same thing about the wealthy. And about two-thirds (67%) of respondents think it is fair to tax rich people at a higher rate than ordinary people in order to help pay for government programmes to benefit the poor.

- Trust and integrity of tax authorities: A majority (56%) of Ugandans say that “most” or “all” tax officials are corrupt. Only about one-third (35%) say they trust the Uganda Revenue Authority “somewhat” or “a lot.”

- Difficulty in accessing tax information: Three-fourths (76%) of Ugandans say it is “difficult” or “very difficult” to find out what taxes and fees they are supposed to pay. An even larger majority (83%) report that it is hard to find out how the government uses the tax revenues it collects.

- Taxes and government accountability: Fewer than half (46%) of Ugandans believe that their government usually uses tax revenues for the well-being of its citizens. Two- thirds (66%) want Parliament to monitor how tax revenues are spent.

- Tax avoidance: About one-third (35%) of citizens say that people in their country “often” or “always” avoid paying taxes they owe, a 14-percentage-point increase from 2012 (21%).

- Support for taxing the informal sector: Fewer than four in 10 citizens (38%) say the government should make sure that small traders and others in the informal sector pay taxes, while a majority (58%) disagree.

- Explaining popular support for broadening the tax base in the informal sector: Institutional performance, perceived fairness of the tax system, and access to tax information play as important a role as people’s personal circumstances.

Governments rely on tax revenue to finance investments in human capital, infrastructure, and public services for their citizens. The quality of government services and a country’s development can be jeopardized if taxes are not collected, are squandered, or are misappropriated by the government.

According to statistics from the Uganda Revenue Authority (URA), about 2.6 million Ugandans were registered taxpayers as of September 2022, but only about 1 million Ugandans are actively paying taxes (Kayiwa, 2022; Oketch, 2021). Analysts attribute the low tax-revenue collections to inadequate administrative capacity, weak checks and balances, and a lack of social norms for tax compliance, among other factors (Lakuma & Lwanga, 2017).

Even so, during the 2021/2022 financial year, the URA collected 21.7 trillion Ugandan shillings (UGX) (USD 5.9 billion), its highest-ever revenue collection, reflecting a 12% increase over the previous year. This amount fell just short of the target of UGX 22.4 trillion (Wanyenze, 2022). However, there is little cause to celebrate, for several reasons.

First, Uganda’s ratio of taxes to gross domestic product (GDP) is still very low. In 2020, it stood at 11%, far below the African average of 16% and worse than regional peers Kenya (15.3%) and Rwanda (16.9%). This ratio improved slightly in 2021, to 12.9%, but still fell short of what is required for a country to be self-reliant or economically independent (Organisation for Economic Co-operation and Development, 2022). To increase tax collection, the Ugandan government implemented a domestic revenue mobilization strategy covering the period 2019/2020-2023/2024. Over the course of this five-year plan, the URA is expected to collect revenues totaling between 16% and 18% of GDP. However, the target appears far from achievable, at least in the eyes of tax authority officials (Independent, 2021).

Second, the country’s fiscal deficit and debt burden are both worsening (Bulime & Nakato, 2022).1 While some analysts contend that Uganda’s debt is manageable, sustainable, and safe, others argue that the country lacks a credible fiscal strategy for debt and deficit reduction (Nakato & Bulime, 2022).

As Uganda contends with a low tax-to-GDP ratio as well as a growing fiscal deficit and debt burden, it becomes even more important for the country to increase its tax base and improve tax compliance among citizens.

In this policy paper, we seek to provide insights into whether Ugandans perceive their tax system to be legitimate and fair and the extent to which citizens trust the Uganda Revenue Authority. We describe taxpayers’ views on tax compliance and support for taxation of the informal sector and examine factors that shape these attitudes. For most of this analysis, we draw on data from the Afrobarometer Round 8 survey in 2019, which included a special module on taxation. For some of Afrobarometer’s standard tracking questions, such as on institutional trust and corruption, we also bring in data from previous survey rounds as well as the most recent survey completed in 2022 (Round 9).

Overall, our findings show that a majority of Ugandans endorse their government’s right to collect taxes. However, this perceived legitimacy has declined substantially over the past decade, whereas the perception that people often avoid paying their taxes has increased.

Moreover, most Ugandans question the fairness of their country’s tax system, see tax officials as corrupt and untrustworthy, and say they find it difficult to get information about tax requirements and uses. Fewer than half think their government uses tax revenues for the well-being of citizens.

For instance, the fiscal deficit increased from UGX 9.9 trillion (USD 2.7 billion) in 2019/2020 to UGX 13.5 trillion (USD 3.68 billion) in 2020/2021. Meanwhile, over just five years, the country’s debt increased from UGX 29.6 trillion (USD 8.06 billion), or 34.6% of GDP, to UGX 69.5 trillion (USD 18.92 billion), or 47% of GDP, in 2020/2021 (Bulime & Nakato, 2022).

Our study also reveals that perceptions of corruption among tax officials, improper use of tax revenue, unfair taxation of ordinary citizens, and difficulty in accessing tax-related information significantly undermine public support for broadening the tax base in the informal sector.